Does Applying for Truck Financing Hurt Your Credit Score?

This is one of the first questions I hear from almost every driver who calls in. And honestly, I get it. You've heard the horror stories.

A buddy goes to a dealership to look at a truck, fills out one application, and two weeks later, he's got 6, sometimes 10 hard inquiries on his credit report. His score drops 30- 50 points before he gets the truck, and the sad part is that the dealership does not care.

That's not how we do things. Because we went through that and didn't like what industry did. But let me explain why, because the difference actually matters more than most people realize.

Hard Pulls vs. Soft Pulls: What's the Difference?

A hard credit pull is what happens when a lender runs your credit with the intent to make a lending decision. Every hard pull gets reported to the credit bureaus. One or two won't kill you, but stack five or six in a short window and your score starts bleeding and stays there for years.

Lenders see that and start asking questions. Why is this person shopping so hard? Are they desperate? It creates a bad look even if your credit is solid, and doesn't help you at all.

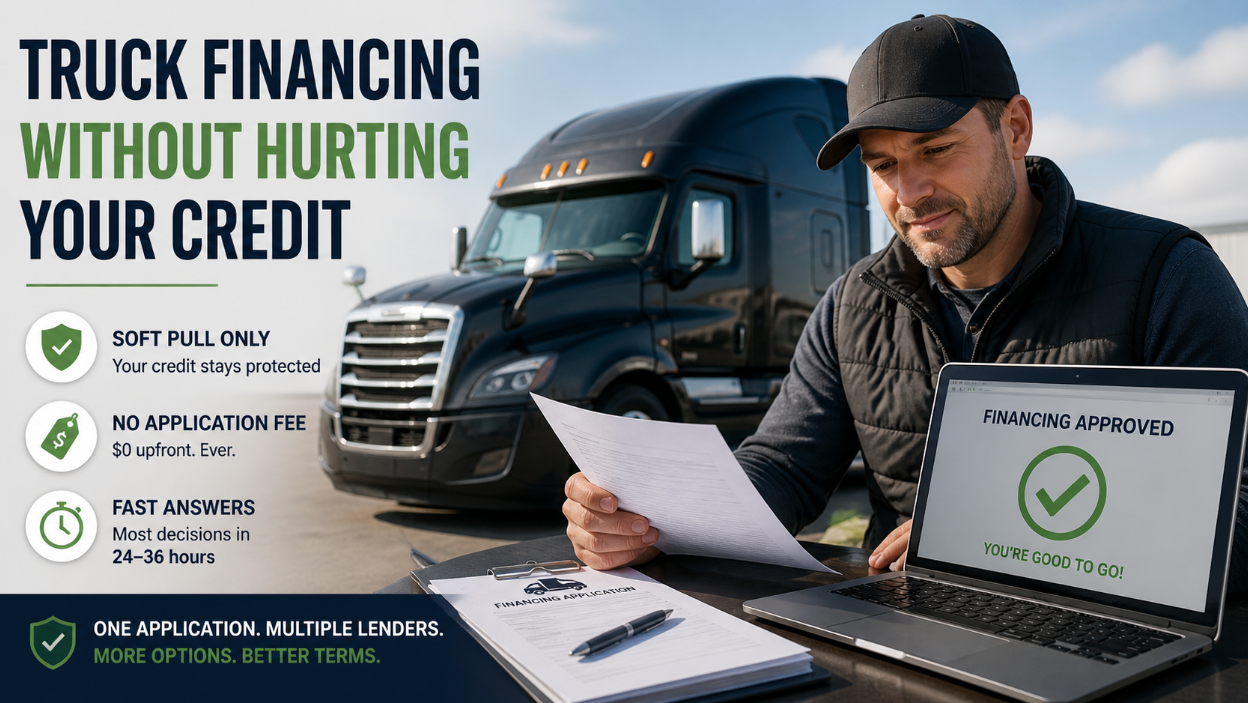

A soft pull is different, and it makes more sense; it lets us see your credit profile without triggering a hard inquiry. Your score stays exactly where it is. The bureaus don't report it. Other lenders can't even see that it happened.

We're licensed to run soft credit pulls. So when you apply with us, your credit score doesn't move. Not a single point. We are taking the extra step to make sure our clients receive some of the best service in the market.

Why This Matters More Than You Think

Here's where it gets real. Say you're a first-time owner operator sitting at a 640-670 credit score. That's still workable if you know how to structure deals. We can get you into a truck financing with that score, and you may need some down payment.

But if you went to three dealerships first and each one ran a hard pull, now you're sitting at 615 or 620. That 20-point drop just changed your rate. It might have changed your approval entirely, and you have a lower chance of getting the loan, or at least a decent rate.

I've seen this happen. A driver calls us after shopping around, and by the time he gets to us, his credit has already taken hits from other dealer applications. We can still work with it, but the terms aren't what they would have been if he'd come to us first, time lost and credit destroyed for 12-24 months..

So does it matter where you apply first? Yeah. It really does, because we know how to do this job professionally and to provide good service.

Does Applying for Truck Financing Hurt Your Credit Score

There's No Application Fee Either

While we're on the subject, let me clear this up too. We don't charge an application fee. Zero. Nothing upfront. You fill out a one-page application through DocuSign, send us your documents, and we go to work.

Some lenders and brokers charge $200, $500, or even more just to look at your file. I never understood that mode, but that's how they operate. You're asking a driver to pay money before he even knows if he qualifies? That's backwards. I had a trucking company, and I understand how hard the industry is.

Our process is simple. You apply, we pull a soft credit check, we package your file, and we submit it to multiple lenders at the same time. If you get approved (and most people who meet the basic requirements do), then we move forward. If not, you haven't lost a dime, and your credit is untouched, and we tell you in 24-36 hours.

What We Actually Look At

When your application comes in, we're building three profiles on you. Personal credit profile, business profile, and financial profile. The soft pull gives us the credit picture. Then we look at your bank statements to see what's flowing through your account, your time in business, how many trucks you're running, and whether you've taken on a bunch of new debt recently, and how you paid your existing loans.

Lenders want to see stability. Money coming in, money going out in a way that makes sense, and enough in the bank to show you're not living load to load. For a first-time buyer, having at least $10,000 in the bank for at least 3 months goes a long way. It tells the lender you're serious, and you've been planning this, and you are reliable enough to trust you with their money.

(If your books are messy or you're running a lot of cash through personal accounts, that's a separate conversation. But it's one worth having before you apply anywhere, we always try to make sure that you get the best results)

One Application, Multiple Lenders

This is the other piece that surprises people. When you apply with us, we're not sending your file to one bank and crossing our fingers.

We create your profile and submit to multiple lenders simultaneously, so that they all can access your file through our cloud and underwrite the deal. That means you might get two or three offers back and actually pick the one that works best for your situation.

Try doing that at a dealership. You can't. They run your credit, send it to their one or two financing partners, and you get what you get.

With us, we have about 40 lenders in our network. And because we used a soft pull upfront, your credit didn't take a hit from any of it, because we have a system.

Want to buy three trucks at once? We can run separate approvals through different lenders for each one. I've had clients do exactly that. One application on their end, multiple funded deals on ours.

So Should You Be Worried About Applying?

Not with us. Your credit stays clean, your wallet stays full, and you get a real answer fast. Most approvals for deals under $100,000 come back in 24 to 36 hours. Funding usually takes five to seven days after that, and insurance is typically the only thing that slows it down.

If you've been holding and not applying because you're worried about credit damage or upfront costs, that's not a factor here.

The application is free, the credit check is soft, and the process is built to protect you, not nickel and dime you before anything even happens, you complete the app and we do all the work for you without upfront pay.

Fill out the form at truckingfinanceloans.com and see where you stand. No risk, no cost, no credit damage. Just a straight answer on what you qualify for.